The Finnish economy started to grow towards the end of 2025, and growth continued at the beginning of 2026. The economic outlook is now weakened and clouded by the high uncertainty over the war in Iran.

With the gyrating, generally upward trend in crude oil prices since the outbreak of the Iran war, oil price trends – particularly their impacts on Russian economic output and government finances – deserve consideration.

Due to the higher interest rates, the number of households that considered themselves over-indebted also increased among middle- and high-income households.

It has been over a decade since Russia launched military actions against Ukraine and this week marks the fourth anniversary since the full-scale invasion, yet Ukraine’s economy continues to grow, evolve and even innovate.

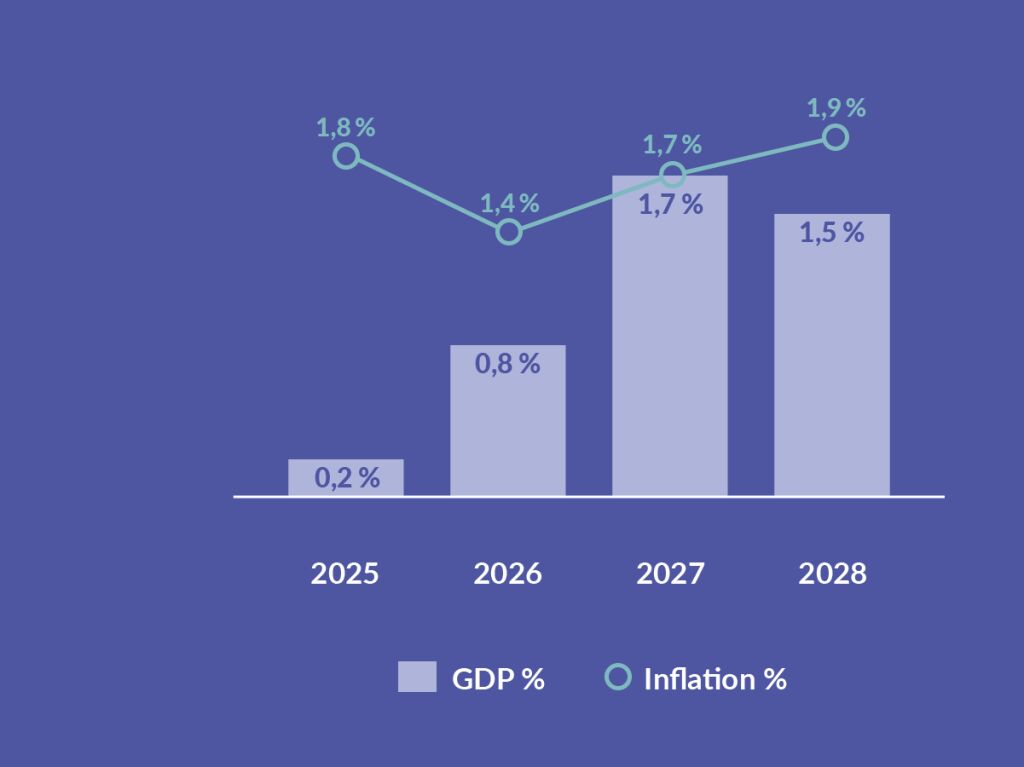

Finland’s economy is emerging from a phase of extremely low growth. Growth in the economy for the full year 2025 will be 0.2%. Growth will rise to 0.8% in 2026 and to 1.7% in 2027. In 2028, the final year of the forecast period, growth will level out at 1.5%.

In this scenario, presented as an alternative to the Bank of Finland’s economic forecast, it is assumed that the economic recovery will be delayed and that growth will be slower than in the baseline scenario. Finland's economy will be almost 2% smaller in 2028 under the alternative scenario than in the baseline scenario.

Finland's public debt is continuing to rise. Turning the debt trajectory onto a declining path more permanently requires time and the entire fiscal policy toolkit. Sustained efforts will produce results if resolute action is taken to achieve the targets while strengthening the economy’s growth potential.

In recent years the Finnish labour market, with declining employment and rising unemployment, has been considerably weaker than the euro area labour market. Both cyclical and structural factors underlie recent labour market developments in Finland and the euro area.

When the Bank of Finland produces forecasts for the Finnish economy, the main tool it uses is Aino, which is a dynamic stochastic general equilibrium (DSGE) model. The article describes the forecasting process, the features of forecasting models and their key role in economic analysis at the Bank of Finland.

Finland’s economy is turning the corner, but slowly. Households are bringing their finances into balance, and both exports and investments will gradually pick up. When growth in the economy strengthens, employment will also improve. Inflation will remain moderate in the immediate years ahead. Finland’s public debt will continue to rise.

Growth in the economy for the full year 2025 will be 0.2%. Growth will rise to 0.8% in 2026 and to 1.7% in 2027. In 2028, the final year of the forecast period, growth will level out at 1.5%.

The latest preliminary budget framework approved by the Russian government suggests a tightening of the government’s fiscal stance. The large war deficits of recent years have complicated Russia’s finances, forcing the government to harness all parts of the economy to finance the war effort.

Defence spending is expected to increase significantly in the euro area in the coming years. Until now, euro area defence spending has mainly consisted of consumption expenditure, such as personnel costs. Growth effects would likely remain temporary and would support a number of specific manufacturing industries.

There are considerable differences between countries of the euro area in the prevalence of variable rate bank loans. According to recent research by the authors, the extent to which bank loans are variable rate loans influences how the key ECB interest rates affect the demand for corporate loans.

Wage inflation is one of the most significant factors affecting consumer price inflation, and its impact is strongest in the service industries. Wage inflation in the euro area is monitored using a variety of indicators that complement each other.

Finland’s economy is still sluggish, but growth is picking up little by little. Due to the economy’s weak performance in the early months of the year, the full-year growth for 2025 will be 0.3%. However, growth will pick up to 1.3% in 2026 and to 1.7% in 2027.

The economy of the euro area has held on this year amid the considerable trade policy and geopolitical uncertainties. The tariff agreement reached by the EU with the United States has reduced the general uncertainty felt by businesses and consumers, but the tariff increases will weaken economic growth.

In early 2025, the Bank of Finland conducted a survey on the prospects, benefits and risks of quantum technology in the financial sector. Based on the survey responses, quantum tech-nology has the potential to reshape business activities significantly in the long term. Only a few tests and practical trials have been conducted so far, however, as the technology is im-mature. As the opportunities of quantum technology, respondents cited the improvement of risk management and information security and the development of investment activities. In-formation security was also highlighted among the risks, however.

In mid-July, European Union countries adopted their 18th sanctions package of economic and individual measures against Russia. The latest batch of sanctions seek to further degrade Russia’s ability to pursue its war of aggression in Ukraine and support EU efforts to end the war.

This website saves on your device small data files known as cookies. These are divided into essential cookies and statistical ones. Essential cookies are always operational, as they allow use of the site and ensure data security.

The site does not use any cookies that identify the user.

Select ‘Approve cookies’ or click ‘Edit cookie settings’, read the additional information and tailor the cookies to your preferences.

Functional cookies

Essential cookies enable the website’s data security and basic functions such as navigating around the site and the search function. Essential cookies do not gather any data that can identify a user of the site.

Statistical cookies

Statistical enhancement cookies help us develop the site to meet users’ needs. They gather data on e.g. users’ terminals, site visits and time spent on the site. Statistical cookies do not gather any data that can identify the user.